Notice:

The Wage Credit Scheme (WCS) has ended. The final WCS payout was made to all eligible employers in March 2022.

IRAS will no longer accept queries on WCS (including requests for payment and breakdown details) from 1 Jan 2023. The WCS helpline will also cease operations from 1 Dec 2022.

For requests relating to payment, please write in to [email protected] by 31 Oct 2022. Requests submitted after the deadline will not be considered. Any unclaimed WCS will be forfeited.

Under the Wage Credit Scheme (WCS) introduced in Budget 2013 and extended in Budget 2015, the Government co-funded 40% of wage increases from 2013-20151 and 20% of wage increases from 2016-2017 given to Singapore Citizen employees who earned a gross monthly wage of up to $4,000. Only employers are eligible for the co-funding.

In Budget 2018, the WCS was extended for three more years, i.e. 2018, 2019 and 2020, to support businesses embarking on transformation efforts and encourage sharing of productivity gains with workers. Government co-funding was maintained at 20% in 2018.

In Budget 2020, the government co-funding ratios for wage increases in 2019 and 2020 were further raised from the current 15% and 10%, to 20% and 15% respectively. The qualifying gross wage ceiling was also raised from $4,000 to $5,000 for both years.

In Budget 2021, the Scheme was further extended by one year with the government co-funding ratio remaining at 15% for wage increases given in 2021, and the qualifying gross wage ceiling maintained at $5,000.

All other qualifying conditions were unchanged.

1 As announced on 11 Sep 2018, requests made after 30 Nov 2018 for the review of wage credit payouts relating to Qualifying Years 2013-2015 are no longer considered.

On this page:

Qualifying Conditions

Who qualified for WCS

All employers giving wage increases to Singapore Citizen employees who:

- Received CPF contributions from a single employer for at least 3 calendar months* in the preceding year2;

- Had been on the employer's payroll for at least 3 calendar months* in the qualifying year3 (i.e. employer must have paid employee CPF contributions for at least three calendar months* in qualifying year); and

- Had at least $50 gross monthly wage increase (up to the Gross Monthly Wage ceiling4)

- Was not the business owner of the same entity (i.e. sole proprietor of the sole proprietorship, or a partner of the partnership, or both a shareholder and director of a company)

*The three months minimum employment duration need not be continuous.

2Preceding year refers to the year before the Qualifying Year in the relevant year of payout.

3Qualifying year refers to the year for which Wage Credit is computed, based on the wage increases given in that year. There were nine qualifying years, i.e. 2013, 2014, 2015, 2016, 2017, 2018, 2019, 2020 and 2021. Wage increases relating to Qualifying Years 2013-2015 were no longer eligible for payouts from 1 Dec 2018.

4In Budget 2020, the qualifying gross wage ceiling was raised from $4,000 to $5,000 for 2019 and 2020.

Local government agencies, international organisations and businesses not registered in Singapore do not qualify for WCS.

See the full employer exclusion list.

Additional Eligibility Conditions

An employer would not be eligible for a payout under any of the circumstances below:

- The employer was an entity with no substantial trade or business;

- The employer had given, in IRAS' opinion, false or misleading information to IRAS in order to obtain a payout or a higher amount of payout;

- The employer (either singly or with another person) had used, in IRAS' opinion, one or more artificial, contrived or fraudulent steps in order to obtain a payout or a higher amount of payout;

- The employer was convicted in the qualifying or preceding year for making CPF contributions to Singaporeans who were not actively employed by the firm

An employer would not be eligible for a payout for a wage increase given to a particular employee who:

- Did not carry out any substantive work for the employer;

- Effectively controlled the employer (i.e. controls decision making power and management of the business or company)

- If the total wages paid by an employer for a period is not commensurate with the volume or nature of activity carried out by the employer in that period, then the employer is only eligible for an amount of payout that, in IRAS' opinion, corresponds to the increase in the total wages that is commensurate with such volume or nature of activity.

- If the total wages paid by an employer to a particular employee for a period is not commensurate with the volume or nature of work carried out by the employee in that period for the employer, then the employer is only eligible, in respect of that employee, for an amount of payout that, in IRAS' opinion, corresponds to the increase in the total wages paid to that employee for that period that is commensurate with such volume or nature of work.

- If an employer had failed to give to IRAS, by the time specified by IRAS, any information requested by IRAS for the purpose of determining the employer's eligibility for a payout or the amount of payout the employer is eligible for, with respect to one or more employees, then the employer would not be given the payout for these employees.

Additional Terms of Disbursement

The Government has the right to withhold, suspend or deny the disbursement of any WCS payout to an employer if the employer was reasonably suspected or found to:

- be ineligible to receive a payout; or

- have carried out or participated in any criminal activity in the course of carrying on its trade or business.

If the employer is reasonably suspected or found to have been ineligible or involved in criminal activity at the time any previous payouts were disbursed, the Government also has the right to recover from the employer an amount equal to any payout disbursed, from the time the employer: (a) was ineligible to receive a payout; or (b) first carried out or participated in the criminal activity.

Here, “criminal activity” means any activity which, if carried out, is a criminal offence (including but not limited to money laundering or vice-related activities), regardless of whether such activity is related to the WCS.

Computation of Wage Credit

Wage Credits on each qualifying employee will be computed as follows:

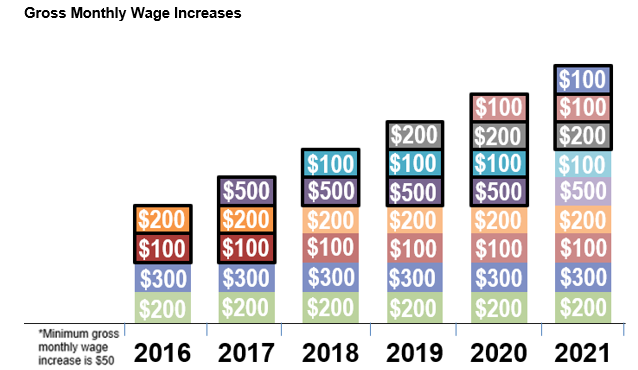

Assume a new employee was hired since 2012 until Sep 2021; and was given gross monthly wage increases of $200 in 2013, $300 in 2014, $100 in 2015, $200 in 2016 and $500 in 2017, $100 in 2018, $200 in 2019 and $100 in 2020 and 2021.

| Under First Extended WCS (2016 - 2017) | Under Second Extended WCS & Budget 2020 (2018 - 2020) | Budget 2021 | |||||

| Year | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | |

| Qualifying Wage Increase | $300 | $800 | $600 | $800 | 900 | $400 | |

| Govt Co-Funding | 20% x $300 = $60/mth | 20% x $800 = $160/mth | 20% x $600 = $120/mth | 15% x $800 = $120/mth | The additional 5% x $800 = $40/mth | 15% x $900 = $135/mth | 15% x $400 = $60/mth |

| Amount of Wage Credit | $60 x 12mths = $720 | $160 x 12mths = $1,920 | $120 x 12mths = $1,440 | $120 x 12mths = $1,440 | $40 x 12mths = $480 | $135 x 12mths = $1,620 | $60 x 9mths = $540 |

| To be Paid in | Mar 2017 | Mar 2018 | Mar 2019 | Mar 2020 | Jun 2020 (Budget 2020 Supplementary payout) | Mar 2021 | Mar 2022 |

Gross Monthly Wage = Total wages (basic salary and additional wages such as overtime pay and bonuses) paid by the employer to the employee in a calendar year / Number of months in which CPF contributions were made.

As announced by the Government on 8 April 2021, excess Jobs Support Scheme (JSS) payouts were credited to some businesses in October 2020 due to errors in the reopening dates used to determine the JSS payouts. Affected businesses have been informed directly. Businesses with excess JSS amounts outstanding might have these offset against future WCS payouts if eligible. Please write in to [email protected] if you wish to make payment arrangements to return the excess JSS payout.

Receiving Wage Credit

Application was not required. IRAS notified eligible employers by post of the Wage Credit payable to them by end Mar of the payout year.

When is the payout

Payouts were given to employers by 31 Mar of the payout year.

How do employers receive the payout

In line with Singapore’s Smart Nation efforts, all WCS payouts were disbursed through either GIRO or PayNow Corporate. No cheques were issued for the payouts.

Payouts were automatically credited to employers' GIRO bank account for Income Tax/GST. For those without GIRO accounts, the payout were credited to their bank accounts that were registered with PayNow Corporate5. Employers who were not already on these direct crediting modes would have to sign up for these modes to receive their payouts.

5Organisations can sign up for PayNow Corporate by linking their organisation’s UEN (without suffix) [e.g. ROC (2019XXXXXA), ROB (531XXXXXA), UEN (T19LLXXXXA)] to their bank account via internet banking. The nine banks participating in PayNow Corporate are United Overseas Bank, DBS Bank/POSB, OCBC Bank, Citibank, HSBC, Maybank, Standard Chartered Bank, Bank of China and Industrial and Commercial Bank of China Limited. For assistance, please approach these banks.

Is the Wage Credit payout taxable?

The Wage Credit payout was a government grant that co-funded wage increases given to your employees. Hence it was considered revenue that was taxable in the hands of the employers. The payouts were taxed in the relevant Year of Assessment corresponding to the year you received the payouts.

Individuals (including sole-proprietors) and partnerships were not required to declare the Wage Credit payout received in their income tax returns (Form B/B1 or Form P) as this was automatically included by IRAS in their tax assessments for the relevant YA.

Companies were however, required to declare the Wage Credit payout received in their income tax return (Form C/Form C-S) for the relevant YA.

Submitting a Request for Wage Credit Breakdown

Please note that IRAS no longer accepts requests for breakdown details.

Appealing for Wage Credit Adjustment

The last date to submit an appeal was 30 Jun 2022.

Background and Contact Information

Background of the Scheme

The Wage Credit Scheme (WCS) was part of the 3-Year Transition Support Package introduced in Budget 2013.

As announced in Budget 2015, the Government extended the WCS for two more years, i.e. 2016 and 2017, to give firms more time to adjust to rising wages in the tight labour market.

In Budget 2018, the WCS was extended for three more years, i.e. 2018, 2019 and 2020, to support businesses embarking on transformation efforts and encourage sharing of productivity gains with workers.

In Budget 2020, the government co-funding ratios for wage increases in 2019 and 2020 were further raised from the current 15% and 10%, to 20% and 15% respectively. The qualifying gross wage ceiling was also raised from $4,000 to $5,000 for both years.

In Budget 2021, the Scheme was extended by one year, with the government co-funding ratio remaining at 15% for wage increases given in 2021, and the qualifying gross wage ceiling maintained at $5,000.

Through WCS, businesses affected by economic restructuring received Government support to manage rising labour costs. The payouts allowed businesses to free up resources to make investments in productivity and share the productivity gains with their employees.

Contact IRAS

Email us: [email protected]

FAQs

A. General Questions on the Scheme (8)

What is the Wage Credit Scheme (WCS) and its objectives?

In Budget 2013, the Wage Credit Scheme was introduced as a three-year Scheme under which the Government co-funded 40% of the wage increases given to Singapore Citizen employees earning a gross monthly wage of not more than $4,000 over the period 2013 to 2015.

In Budget 2015, the Scheme was extended for two more years, i.e. 2016 and 2017. Wage increases given to Singapore Citizen employees earning a gross monthly wage of not more than $4,000 in 2016 and 2017 were co-funded at 20% instead of 40%. In addition, gross monthly wage increases (at least $50) previously given in 2015 and 2016 by the same employer were co-funded at 20% if they were sustained in 2016 and 2017.

In Budget 2018, the WCS was further extended for three more years, i.e. 2018, 2019 and 2020, to support businesses embarking on transformation efforts and encourage sharing of productivity gains with workers. Government co-funding was maintained at 20% in 2018. Subsequently, the co-funding ratio stepped down to 15% in 2019 and 10% in 2020.

In addition, gross monthly wage increases (at least $50) given in 2017, 2018 and 2019 by the same employer would continue to be co-funded at their respective level of co-funding if they are sustained in 2018, 2019 and 2020.

In Budget 2020, the government co-funding ratios for wage increases in 2019 and 2020 were raised from the current 15% and 10%, to 20% and 15% respectively. The qualifying gross wage ceiling was also raised to $5,000 for both years, up from the current $4,000.

During this period of economic restructuring, businesses could face a tight labour market with rising wages. Through the Scheme, the Government provides businesses with co-funding support for wage increases made to their employees. This would allow businesses to free up resources to invest in productivity, and to share productivity gains with their employees.

In Budget 2021, the WCS was further extended by one year for wage increases given in 2021. Gross monthly wage increases (at least $50) previously given in 2019 and 2020 by the same employer will continue to be co-funded at the respective levels of co-funding if they are sustained in 2020 and 2021.

Who will qualify for the Wage Credit Scheme?

Employers qualify for Wage Credits if they fulfil the following:

- Gave at least a $50 increase in gross monthly wage to Singapore Citizen employees earning up to the Gross Monthly Wage ceiling*;

- Made CPF contributions for these employees for at least three months** in the year of the wage increase ("qualifying year"); and

- The employees who received the wage increase must have received CPF contributions for at least three months with one employer in the preceding year.

*As announced in Budget 2020, the qualifying gross wage ceiling was raised from $4,000 to $5,000 for 2019 and 2020.

**The three months minimum employment duration need not be continuous.

Please refer to Wage Credit Scheme website / Qualifying Conditions.

Why was the Wage Credit Scheme extended? What are the changes under the extended Scheme?

The WCS was extended to help firms cope with near-term cost pressures as they embark on transformation efforts, and to encourage employers to share productivity gains with workers.

Government co-funding was maintained at 20% in 2018. Subsequently, the co-funding ratio stepped down to 15% in 2019 and 10% in 2020. It was then raised to 20% and 15% for 2019 and 2020 respectively as announced in Budget 2020.

In addition, gross monthly wage increases (at least $50) given in 2017, 2018 and 2019 by the same employer would continue to be co-funded at their respective level of co-funding if they were sustained in 2018, 2019 and 2020.

In Budget 2021, the co-funding ratio was maintained at 15%, and the gross monthly wage increases (at least $50) previously given in 2019 and 2020 by the same employer will continue to be co-funded if they are sustained in 2020 and 2021.

Is the Wage Credit Scheme a permanent Scheme?

The Wage Credit Scheme aims to provide transitional support to help businesses cope with near-term pressures as they embark on transformation efforts. It is not a permanent Scheme.

How does the Government know the wages that I pay my employees? Is it necessary for the company to give a wage increment to the employees?

The wages are derived from the compulsory CPF contributions that the employer makes for the employee.

Where there are irregular or significant changes to the CPF contributions made, IRAS may carry out investigations before or after the payouts, to check on the authenticity and correctness of any employee and the wages. Any attempt by the employer to abuse the Scheme to receive Wage Credit payout or to obtain excessive payout will be dealt with seriously.

Wages are determined by the market. It is ultimately for the employers to decide how much pay increase, if any, to give, and to consider the sustainability of the increased wages in subsequent years.

Why was the co-funding at 40% from 2013 to 2015, 20% from 2016 to 2019 and only 15% in 2020 and 2021?

A 40% co-funding for wage increases given from 2013 to 2015 was to provide significant help to employers, while ensuring that they bear a sufficiently large portion of the increase in the long term after the Scheme ended.

The co-funding was reduced to 20% from 2016 to 2019 and further tapered to 15% in 2020 and 2021 to phase out the wage support gradually.

If I meet the qualifying conditions, am I legally entitled to a payout?

Wage Credit is a cash grant to employers who meet the Scheme's qualifying criteria. It is not paid pursuant to any legislation or in connection with any legal obligation of the Government, and hence no employer has an absolute right to any cash payment under the Scheme.

How does the Government ensure that the wage increases I give my employees can be sustained after the Scheme ends?

Under the Scheme, the larger proportion of the wage increase is borne by the employer to ensure sustainability of the increased wage in subsequent years. We encourage businesses to take advantage of the suite of productivity measures offered by the Government to improve their productivity. The Wage Credit payouts help businesses upgrade and retain their workers before their productivity investments take off. This would help businesses ensure that the wage increases given to their employees are sustainable over the longer term.

B. How the Scheme Works (8)

Why is the Wage Credit computed based on the gross monthly wage instead of basic wage of an employee? Why is the qualifying wage only up to $5,000?

Consistent with the flexible wage system, employers can choose whether to increase wages through the basic or variable components of salary, or both. Businesses, especially SMEs, welcome the flexibility as they practise diverse compensation approaches.

With the cap at a wage level of $5,000 the scheme benefits the majority of the lower and middle income group of Singapore Citizens.

If my employee’s gross monthly wage was reduced in 2020 but subsequently increased in 2021, would I be eligible to receive the Wage Credit payout for Qualifying Year 2021?

Yes, provided the increase in the gross monthly wage from 2020 to 2021 was at least $50.

If my employee worked for me for four months in 2021, how is his gross monthly wage computed and how is the Wage Credit computed?

His gross monthly wage will be calculated from the total wages that you paid him in 2021 divided by 4, which is the number of calendar months in which his CPF contributions were made by you in 2021. If there is any increase, of at least $50, in the gross monthly wage over his gross monthly wage in 2020, you will receive Wage Credit for the qualifying year 2021 (to be paid in Mar 2022 based on 15% of his increase in gross monthly wage), for the 4 months.

My employee joined the company in Nov 2020 but left in Feb 2021. As he had been employed by the company for a total of four months, will my company qualify for Wage Credit in qualifying years 2020 and 2021?

No, your company will not qualify for Wage Credit in qualifying years 2020 and 2021 as the employee was employed by your company for less than three months in 2020 and less than three months in 2021.

I have recruited a new employee from Feb 2021 who had worked with two different employers in 2020 (each more than three months). How would the Wage Credit be computed assuming his gross monthly wage in 2021 is $2,500 and the gross monthly wages in 2020 was $2,000 under employer A and $2,100 under employer B?

The highest of the employee's previous gross monthly wages will be used to compute the Wage Credit, which in this case is $2,100 under employer B.

Wage Credit for QY2021:

Mar 2022 Payout = 15% of ($2,500 - $2,100) X 11 months = $660

If I paid my employee a bonus for his 2020 performance in 2021, will the bonus be considered in the computation of my employee’s gross monthly wage for 2020 or 2021?

The bonus will be reflected in the employee's gross monthly wage for 2021, i.e. the year in which the payment was made.

I have increased the hourly wage of my hourly-rated employee who has now chosen to work fewer hours each month. How would the Wage Credit be computed?

Wage Credit is computed based on the increase in the gross monthly wage. For hourly-rated employee, the gross monthly wage has to take into account the hourly wage and the actual number of hours worked. Hence even if the hourly wage might have increased, there might not be an increase in the gross monthly wage if the employee has chosen to work fewer hours each month.

My employee worked for another firm that gave him a $300 raise in gross monthly wage since Jan 2020 to a revised gross monthly wage of $2300. I paid him the same gross monthly wage of $2,300 when he joined me in 2021. Will I be entitled to the Wage Credit on the ‘sustained’ gross monthly wage increase of $300 in 2021?

No, because the $300 gross monthly wage increase was given by a different employer. There was no sustained wage increase given by you.

C. Eligibility Criteria for Employees (8)

Are part time and contract workers covered by the Scheme?

Yes, all part-time, hourly rated, contract and full-time employees are covered by the Scheme, as long as they are paid CPF contributions by their employer.

I own a business and am paying CPF contributions to myself. Will I qualify for the Wage Credit?

No. The following individuals will not qualify as employees under the Wage Credit Scheme:

- Sole proprietors and partners of general partnerships/ limited liability partnerships/ limited partnerships.

- Employees who are both shareholders and directors (as defined in Section 4(1) of the Companies Act) of the company they are employed in, or employees who are both members and directors in the case of a company limited by guarantee.

- Self-employed individuals including but not limited to commission agents, taxi-drivers, owners of professional practices.

The Wage Credit Scheme aims to encourage employers to share productivity gains with their employees. As the individuals listed above are also owners/ members/ directors of the company or business, they are not considered employees for the purpose of the Wage Credit Scheme.

I am a self-employed or a business owner. If I were to work for another firm in 2021, will the firm be able to benefit from the Wage Credit by employing me?

You will be a new hire with no previous employment to consider when computing the preceding year's gross monthly wage. Hence, no Wage Credit can be derived in your first year of employment with the firm.

My new employee previously worked for an employer who is on the employer exclusion list. Will I be able to qualify for Wage Credit?

Yes, you will be able to qualify for Wage Credit based on the increase in the gross monthly wage over his previous year's gross monthly wage, even though his previous employer was on the employer exclusion list.

Will employers qualify for Wage Credit for new hires?

The Government recognizes that there will be job switching during the qualifying years period. Employers hiring new employees will benefit from the Scheme in the year of hire as long as the employee had worked for at least three calendar months with the same employer (need not be you) in the previous year, and the new employer pays him a gross monthly wage of at least $50 more than his previous employer in the previous year. This wage increase will be computed automatically based on the employee's CPF contribution records, and Wage Credit will be paid out to the employer if all conditions of the Scheme are met.

My employee was hired in Jan 2019 and she was on no pay leave for the whole year in 2020 before returning to work in 2021. Will I be able to qualify for Wage Credit in qualifying year 2021?

Yes, you will qualify for Wage Credit in qualifying year 2021 based on the wage increase you gave the employee in 2021 over 2019. This is provided that the employee had worked with you for at least three calendar months in 2019 and 2021 and did not seek active employment while on no-pay leave.

Our company has a Singapore Citizen employee who is working at an overseas branch of my company, or has been seconded to another company in Singapore. Will our company be eligible for the Wage Credit?

The payout will be given to the employer who has made the CPF contribution for the said employee. The same applies to any other employment arrangements. The payout will only be given to the employer who has made the CPF contribution based on the CPFB's record.

So long as your company is not on the employer exclusion list, you may appeal for Wage Credit for your Singaporean employees who are posted to an overseas branch or seconded overseas, even though the company does not have to pay CPF contributions for these employees.

Will I qualify for Wage Credit if I receive Senior Employment Credit (SEC) for an employee?

Yes, an employer may qualify for both SEC and WCS for an employee. The two Schemes serve different purposes. The SEC Scheme provides businesses with support to hire older Singaporean workers while the WCS supports businesses embarking on transformation efforts and encourage sharing of productivity gains with workers.

D. Eligibility Criteria for Employers (5)

Are non-profit organisations registered in Singapore eligible for the Scheme?

Yes, public companies limited by guarantee, societies and charities and institutions of a public character are eligible for the Scheme if they make CPF contributions for their employees.

Are companies co-funded by the Government eligible for the Scheme?

Yes, if they are not listed in the exclusion list.

Will I qualify for Wage Credit if the training for employees is funded by Workforce Development Agency (WDA)?

Yes, as long as the employer had made CPF contributions to the employee for the wages paid to the employee, and the rest of the eligibility criteria are satisfied, the employer will qualify for Wage Credit for this employee.

I gave a wage increase to my employee in the qualifying year 2021, but my business was closed down during the year. Will I be receiving the WCS Payout in Mar 2022?

The gross monthly wage and the Wage Credit for the qualifying year 2021 can only be computed after the end of the year 2021, and the payout will only be disbursed to the registered business entity in Mar 2022. If your business entity had already been deregistered in Mar 2022, it will not receive the WCS payout.

If I engage a third-party contractor to hire my workers, will I benefit from the WCS? Can the contractor transfer the Wage Credit to me?

The Wage Credit is paid to the employer registered with CPF Board, and is taxable.

If the third-party contractor is the registered employer, he will receive the WCS payout. Whether the Wage Credit is to be shared between you and the third-party contractor is a private arrangement between both parties.

If the contractor transfers part or all of the Wage Credit to you, the amount received by you would correspondingly reduce your manpower cost allowed for tax deduction.

E. What Employers Need to Do (7)

Do I need to apportion the gross monthly wage if the employee is remunerated based on the working days?

No. The gross monthly wage is computed based on the CPF contributions you make for the employee.

What is the cut-off date for employers to make CPF contributions to qualify for Wage Credit?

As per CPF requirements, CPF contributions for each month are due at the end of each month. However, employers have a grace period of 14 days to pay CPF contributions after the end of the month. If the 14th day falls on a Saturday, Sunday or Public Holiday, the grace period will be extended to the next working day.

Employers should thus ensure that all CPF contributions on wages are paid by the 14th of the following month.

Will late CPF contributions and adjustments to CPF contributions be accepted for the Scheme?

For each qualifying year, the deadline for late contributions/adjustments in relation to wages paid in the qualifying year is 14 Jan of the subsequent year. If 14 Jan falls on a Saturday, Sunday or Public Holiday, the deadline will be extended to the next working day. All late contributions/adjustments paid after this deadline will not be used in the computation of Wage Credit. The usual penalties apply to late CPF contributions.

Is there a minimum Wage Credit before payment is made?

For employers who have a GIRO bank account with IRAS (for Income Tax or GST), or have registered with PayNow Corporate [by linking the organisation’s UEN (without suffix) to the bank account], their Wage Credit will be credited directly into the account regardless of the amount.

Is the Wage Credit taxable? Why?

The Wage Credit payout is a government grant that co-funds wage increases. Hence, it is considered a revenue that is taxable in the hands of the employers.

When will the Wage Credit be taxed and do I need to declare the Wage Credit received in my Tax Return?

The payouts will be taxed in the relevant Year of Assessment corresponding to the year you received the payouts. Payouts may be used to offset any of your outstanding tax.

Individuals (including sole-proprietors) and partnerships are not required to declare the Wage Credit Scheme payout received in their income tax returns (Form B/B1 or Form P) as this will be automatically included by IRAS in their tax assessment for the relevant YA.

Companies are however, required to declare the Wage Credit Scheme payout received in their income tax return (Form C/Form C-S) for the relevant YA.

What if my company name changes during the qualifying year?

If the UEN of the business is unchanged, Wage Credit will automatically be paid out to the same UEN. If the UEN of the business changes, the business can appeal to IRAS to amalgamate the records of the old UEN with the new UEN. The employer may submit an appeal and it will be considered on a case-by-case basis, to establish if there is indeed a transfer of rights and obligations.