PWCS Eligibility Checker & Breakdown Request

Announcement:

A. PWCS Enhancements

As announced at Budget 2026, PWCS will be enhanced as follows:

1) Increased PWCS Co-Funding Support for Qualifying Year 2026

For wage increases given in the qualifying year 2026, the PWCS co-funding support will be raised from 20% to 30% (see Table 1). This enhanced co-funding rate will also apply to wage increases given in qualifying year 2025 and sustained in 2026.

2) Extension of PWCS to 2028

The PWCS will be extended for a further 2 years, from 2026 to 2028. For wage increases given in the qualifying year 2027, the PWCS co-funding support of 30% will continue to apply. For wage increases given in the qualifying year 2028, the PWCS co-funding support will be 20%.

3) Revision to Minimum Qualifying Wage Increase from 2027

For qualifying years 2027 and 2028, the minimum qualifying wage increase will be raised from $100 to $200.

B. March 2026 Payout

If your company has an existing GIRO arrangement as at 18 Mar 2026 with IRAS or is registered for PayNow Corporate as at 26 Mar 2026, you will receive a payout titled “Progressive Wage Credit Scheme” (GIRO) or “GOVT” (PayNow Corporate) in your bank account from 31 Mar 2026. There will not be any PWCS payout made via cheques.

The Progressive Wage Credit Scheme (PWCS) was introduced in Budget 2022 to provide transitional wage support for employers to:

- Adjust to mandatory wage increases for lower-wage workers covered by the Progressive Wage Model and Local Qualifying Salary requirements; and

- Voluntarily raise wages of lower-wage workers.

The Government will co-fund wage increases of eligible resident employees from 2022 to 2028. Employers do not need to apply for the PWCS and can expect to receive the payout for the respective year by the first quarter of the following year.

On this page:

Design of PWCS

The PWCS has the following design:

a) Applies to wage increases given to Singapore Citizen and Permanent Resident employees.

b) Support for wage increases up to $3,000 gross monthly wage ceiling will run from 2022 to 2028. The Government will provide support for wage increases at the stipulated co-funding levels from 2022 to 2028 (see Table 1).

c) Average gross monthly wage increase must be at least $100 in qualifying years 2022 to 2026, and at least $200 in qualifying years 2027 and 2028, to be eligible for PWCS.

d) Eligible wage increases in each qualifying year will be co-funded for two years. For example, a 2025 wage increase will be supported in qualifying year 2025, and also in 2026 if sustained.

e) Employees’ average wage must be $4,000 or lower to be eligible for PWCS. A wage cut-off for PWCS eligibility will apply from 2024 onwards. Employees whose average monthly wage exceeds $4,000 post-wage increase will not be eligible for PWCS.

Qualifying conditions

Is my firm eligible?

Your firm will automatically qualify if you give wage increases to resident1 employees who:

1. Received CPF contributions from a single employer for at least 3 calendar months* in the preceding year2,

2. Have been on your firm’s payroll for at least 3 calendar months in the qualifying year3 (i.e. you must have paid your employee CPF contributions for at least 3 calendar months* in qualifying year), and

3. Have an average gross monthly wage increase of at least $100 for qualifying years 2022 to 2026, and gross monthly wage increase of at least $200 for qualifying years 2027 and 2028

* The 3 calendar months of CPF contributions in the year need not be consecutive.

1Singapore Citizen and Permanent Resident

2Preceding year refers to the year before the qualifying year.

3Qualifying year refers to the year for which the wage credit is computed, based on the wage increases given in that year. The Scheme has 7 qualifying years: 2022, 2023, 2024, 2025, 2026, 2027 and 2028.

Local government agencies, businesses not registered in Singapore, foreign high commissions, embassies, trade offices and international organisations do not qualify for PWCS.

Wages paid to business owners i.e. sole proprietors of sole proprietorships, or partners of a partnership, or both a shareholder and director of a company, will not be eligible for PWCS.

See the full employer exclusion list.

Computation of Progressive Wage Credit

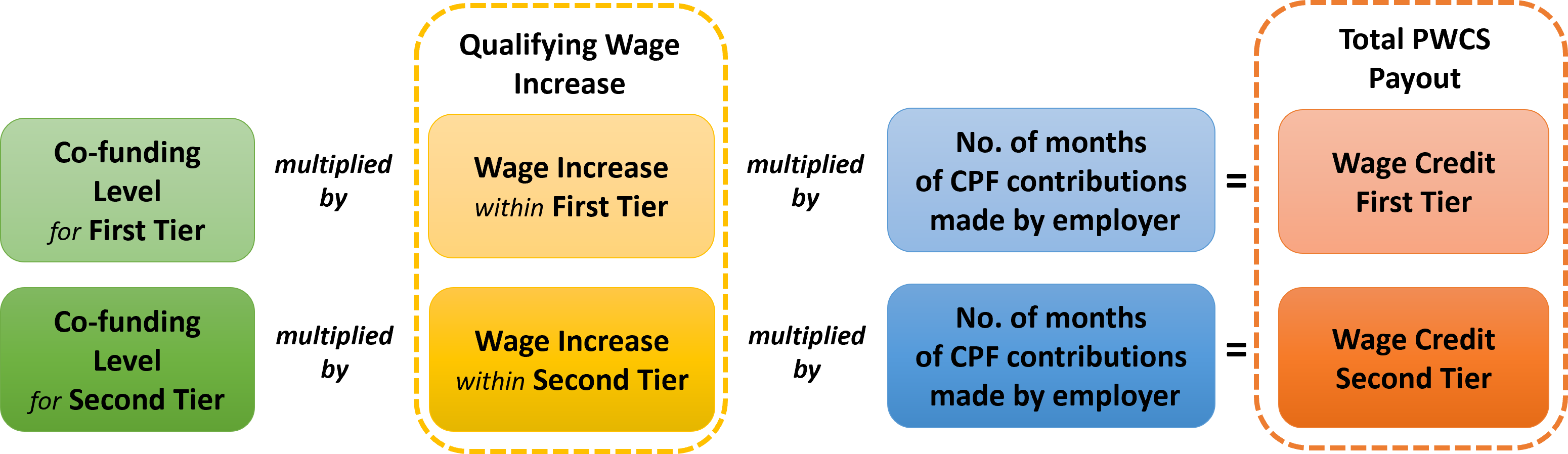

For qualifying years 2022-2024, the Progressive Wage Credit for each eligible employee will be computed as follows:

For qualifying years 2025-2028, the Progressive Wage Credit for each eligible employee will be computed as follows:

Table 1: PWCS co-funding levels for wage increases

| Qualifying Year | First Tier Gross Monthly Wage Ceiling ≤ $2,500 | Second Tier Gross Monthly Wage Ceiling > $2,500 and ≤ $3,000 |

| 2022 | 75%1 | 45%1 |

| 2023 | 75%2 | 45%2 |

| 2024 | 50%3 | 30%3 |

Single Tier Gross Month Wage Ceiling ≤ $3,0004 | ||

| 2025 | 40%5 | |

| 2026 | 30%6 | |

| 2027 | 30%6 | |

| 2028 | 20%6 | |

For the purposes of the PWCS,

Gross monthly wage = Total wages (basic salary and additional wages such as overtime pay and bonuses, but excluding employer CPF contributions) paid by the employer to the employee in a calendar year / Number of months in which CPF contributions were made.

Qualifying wage increase refers to the amount of wage increase given to an employee that qualifies for co-funding in any qualifying year. It consists of two components:

- The gross monthly wage increase given in qualifying year, if it is at least $100 (for qualifying years 2022-2026), and at least $200 (for qualifying years 2027 and 2028)7, and up to the relevant wage ceiling; and

- The gross monthly wage increase given in the preceding year, if it is sustained8

1As announced on 21 Jun 2022, the co-funding support in 2022 has been increased from 50% to 75% for the first tier, and from 30% to 45% for the second tier.

2As announced at Budget 2023, the co-funding support in 2023 has been increased from 50% to 75% for the first tier, and from 30% to 45% for the second tier.

3As announced at Budget 2024, the co-funding support in 2024 has been increased from 30% to 50% for the first tier, and from 15% to 30% for the second tier.

4As announced at Budget 2024, the gross monthly wage ceiling for PWCS co-funding will be increased from $2,500 to $3,000 in qualifying years 2025 and 2026.

5As announced at Budget 2025, the co-funding support in 2025 has been increased from 30% to 40%.

6As announced at Budget 2026, the co-funding support in 2026 has been increased from 20% to 30%.

As announced at Budget 2026, the co-funding support in 2027 will be 30%, and 20% in 2028.

7As announced at Budget 2026, the minimum qualifying wage increase will be raised from $100 to $200 in qualifying years 2027 and 2028. Wage increases below $200 that qualified for PWCS in 2026 and are sustained in 2027 will continue to be co-funded in 2027.

8For qualifying year 2022, there is no sustained gross monthly wage increase in preceding year, as 2022 is the first year of the Scheme. For qualifying year 2028, wage increases will only be co-funded for one year since 2028 is the last year of the Scheme.

Illustrations of PWCS

Example 1: Employee who earns $1,800 per month in 2021, and experiences average gross monthly wage increase of $100 in January of each year from 2022 to 2026, and average gross monthly wage increase of $200 from 2027 to 2028.

Amount of PWCS payout received in total for this employee: $7,620

Note:

[2] Calculation of total PWCS payout for the year assumes that employer makes 12 months of CPF contributions for each qualifying year.

Example 2: Employee who earns $2,200 per month in 2021, and has gross monthly wage increase of $200 in January of each year

Amount of PWCS payout received in total for this employee: $9,360

Note:

[1] As PWCS is effective from 2022, wage increases in 2021 (i.e. increases in 2021 from the 2020 wage) will not be supported by PWCS.

[2] Calculation of total PWCS payout for the year assumes that employer makes 12 months of CPF contributions

for each qualifying year.

Example 3: Employee who earns $4,000 per month in 2021, and has gross monthly wage increase of $100 in January of each year

PWCS will not co-fund the wage increases of this employee, as the employee is already earning above the wage ceiling of $3,000.

Example 4: Employee who earns $2,800 per month in 2023, and has gross monthly wage increase of $1,250 in January of each year

Although the employee’s monthly wage pre-increase is below the wage ceiling of $3,000, PWCS will not co-fund the wage increases of this employee, as the employee’s monthly wage post-increase is above the wage cut-off for PWCS eligibility of $4,000.

Receiving PWCS

Employers do not need to apply for the payouts. For each qualifying year, IRAS will notify eligible employers of the PWCS payout payable to them and disburse the payout by Q1 of the subsequent year. The first payout period for PWCS will be in Q1 2023.

| Qualifying Year | Payout Period |

| 2022 | Q1 2023 |

| 2023 | Q1 2024 |

| 2024 | Q1 2025 |

| 2025 | Q1 2026 |

| 2026 | Q1 2027 |

| 2027 | Q1 2028 |

| 2028 | Q1 2029 |

How do employers receive the payout?

Payouts will automatically be credited to employers' GIRO bank account for Income Tax/GST. For those without GIRO accounts, the payout will be credited to their bank account that is registered with PayNow Corporate1. Employers who are not already on these direct crediting modes will have to sign up for these modes to receive their payouts.

1Organisations can sign up for PayNow Corporate by linking their organisation’s UEN (without suffix) [e.g., ROC (2019XXXXXA), ROB (531XXXXXA), UEN (T19LLXXXXA)] to their bank account via internet banking. The nine banks participating in PayNow Corporate are United Overseas Bank, DBS Bank/POSB, OCBC Bank, Citibank, HSBC, Maybank, Standard Chartered Bank, Bank of China and Industrial and Commercial Bank of China Limited. For assistance, please approach these banks.

Offset of Government scheme overpayments against PWCS payouts

Businesses with overpayments from Government schemes such as Jobs Growth Incentive (JGI) might have these offset against PWCS payouts. Please write to us via myTax Mail if you wish to separately arrange for payment to return the outstanding amounts.

How to request for a breakdown of Progressive Wage Credit?

If you are an employer, you can request for a breakdown of the total Progressive Wage Credit by employee in the year of payout. You can submit an online request via this digital service. We have prepared a step-by-step guide (PDF, 738KB) to assist you. Please note that each qualifying employer is allowed to submit one breakdown request for each qualifying payout.

Receiving the records

If the number of employee records does not exceed 500, they will be mailed to the business's registered address by ordinary mail. If the number of employee records exceeds 500, they will be processed via myTax Mail within ten working days from the date of receipt of the breakdown request.

Contents of the records

The records will provide you with the breakdown of Progressive Wage Credit for your employees. If you have new eligible employees, only their names will be provided, as disclosure of their individual Wage Credits may reveal the wages from their previous employment. If you wish to obtain the individual Progressive Wage Credits of your new employees, they will need to sign a Consent Form (PDF, 186KB), and you will need to complete and submit a Declaration Form within a month from the date of request.

Please note that we will not be able to process the declaration form if you have only one qualifying new employee.

Can employers appeal to qualify for the schemes?

How do I decline PWCS payout?

If you wish to be excluded from current and all future PWCS payouts, please sign up using the Decline PWCS form.

Returning PWCS payouts

To return a PWCS payout that you have received, please do so via internet banking fund transfer. IRAS’ bank account details are as follows:

Payee: IRAS - PWCS TRUST FUND

Account Type: Current Account

Account No.: 072-847500-5

DBS Swift Code: DBSSSGSG

To facilitate the processing of your return, please indicate your business name and purpose (e.g. ABC Pte. Ltd. Decline PWCS) under the “Beneficiary Reference / Purpose of Payment / Remittance Information / Payment Details” field.

Abuse of PWCS

How will the Government detect abuse of PWCS?

The Government takes a serious view of any attempt to abuse the scheme. Offenders may have their PWCS payouts denied and could be charged with offences punishable by penalties, fines and/or imprisonment. To detect potential abuses, the Government has established a robust anti-gaming framework that leverages data from multiple sources to identify risks. When determining whether an arrangement is abusive, the Government will consider all relevant facts and circumstances and conduct in-depth verifications when necessary.

IRAS will only release the PWCS payouts after we are satisfied with the outcome of the review.

Some unacceptable practices include but are not limited to:

Artificially splitting the wages of employees across multiple related business entities

Employers should only make mandatory CPF contributions to employees for the business entities they are working for, instead of artificially splitting the wages of its employees across related business entities to circumvent the PWCS wage ceiling.

Making purported mandatory CPF contributions for non-genuine employees

This is a fraudulent arrangement. Employers should not make any mandatory CPF contributions to individuals who are not their genuine employees. Individuals are reminded that providing their personal information to facilitate such schemes may make them accomplices to the fraud, resulting in criminal liability for the individuals. Individuals should not give out their personal information such as NRIC, Singpass or bank account details in exchange for CPF contributions and/or money.

Making mandatory CPF contributions for purported wages paid without expectation of any work to be done (e.g. solely to fulfil regulatory requirements or quotas, or family members who are not involved in the business)

Employers should only make mandatory CPF contributions to employees for wages paid for work performed as part of a contract of service.

Increasing purported mandatory CPF contributions for employees without any actual wage increase

The prevailing CPF contribution rates can be found on the CPF website.

Inflating purported mandatory CPF contributions and deducting these excess contributions from employees’ wages in cash

This is a fraudulent arrangement. Employers should only make the correct amount of mandatory CPF contributions based on the actual wages paid to their employees.

Making purported mandatory CPF contributions for inflated wages that are not commensurate with the volume or nature of work of the employees

Employers should only make mandatory CPF contributions to employees for wages paid that are commensurate with the volume or nature of work of the employees, instead of making purported mandatory CPF contributions based on inflated wages to increase the amount of the PWCS subsidy.

Continuing purported mandatory CPF contributions for employees who have been retrenched or put on no-pay leave

Employers should stop making mandatory CPF contributions for employees who have been retrenched or are on no-pay leave. However, employers can continue to make voluntary CPF contributions to the CPF accounts of employees on no-pay leave by applying for a separate CPF submission number with CPF Board. (For more details on making voluntary CPF contributions for employees, please find out more at the CPF Board website).

Maintaining purported mandatory CPF contribution amounts based on past wages for employees who have suffered wage cuts

CPF mandatory contributions are based on employees’ wages, age and citizenship. A wage cut on the employees’ part should see a corresponding decrease in the mandatory CPF contributions. However, employers can continue to make voluntary CPF contributions to the CPF accounts of employees whose wages have been cut by applying for a separate CPF submission number with CPF Board. (For more details on making voluntary CPF contributions for employees, please find out more at the CPF Board website).

Contacting IRAS

If you have enquiries that are not addressed on this site, you may either:

- Use our chatbot via the ‘Chat with IRAS’ button located at the bottom right of the website for quick guidance.

- Chat with our live agents online. Our agents are available from 8am to 5pm, Monday to Friday, excluding public holidays.

- Submit an enquiry using our enquiry form at go.gov.sg/askpwcs.

If you are unable to use the above options, you may request a callback via go.gov.sg/callbackegm. Our officers will contact you within two working days.

FAQs

A. General questions on the scheme

1. What is the Progressive Wage Credit Scheme (PWCS) and its objectives?

The PWCS is intended to provide transitional support to employers to:

a. Adjust to mandatory wage increases for lower-wage workers covered by the Progressive Wage Model and Local Qualifying Salary requirements; and

b. Voluntarily raise wages of lower-wage workers.

Employers are to use this period of transition support to invest in upskilling their employees, transforming their businesses and improving productivity to ensure that wage increases remain sustainable in the long-term.

2. Who will qualify for the Progressive Wage Credit Scheme?

Employers will automatically qualify if they are not on the employer exclusion list and wage increases are given to resident employees who:

1. Received CPF contributions from a single employer for at least 3 calendar months* in the preceding year,

2. Have been on the employer’s payroll for at least 3 calendar months in the qualifying year (i.e. employer must have paid CPF contributions to employees for at least 3 calendar months* in qualifying year),

3. Have an average gross monthly wage increase of at least $100 in the qualifying year (for qualifying years 2022-2026) and at least $200 (for qualifying years 2027-2028), and

4. Have wages below the stipulated wage ceilings for PWCS Second Tier (for qualifying years 2022-2024) or PWCS Single Tier (for qualifying years 2025-2028), before the wage increase; and

5. Have an average monthly wage of no more than $4,000 after the wage increase

* The 3 calendar months of CPF contributions in the year need not be consecutive.

3. How is the Progressive Wage Credit Scheme different from the Wage Credit Scheme (WCS)?

The PWCS is a separate scheme from the WCS. The WCS was a transitional scheme intended to support business embarking on transformation efforts and encourage sharing of productivity gains with workers. The PWCS is intended to provide transitional support to employers to:

a. Adjust to mandatory wage increases for lower-wage workers covered by the Progressive Wage Model and Local Qualifying Salary requirements; and

b. Voluntarily raise wages of lower-wage workers.

The WCS has ceased after the last payout for 2021 qualifying wage increases in March 2022.

4. Besides supporting employer in complying with the mandatory Progressive Wages and Local Qualifying Salary, why does the PWCS support voluntary wage increases as well?

The PWCS is intended to provide transitional support to employers to:

a. Adjust to mandatory wage increases for lower-wage workers covered by the Progressive Wage Model and Local Qualifying Salary requirements; and

b. Voluntarily raise wages of lower-wage workers.

This will help us to uplift all lower-wage workers, regardless of whether they are covered by the Progressive Wage Model or Local Qualifying Salary requirements. Hence, the PWCS also supports voluntary wage increases.

5. Why does the PWCS have two tiers in 2022-2024?

While the PWCS is intended to support wage increases for lower-wage workers, we recognise that firms may also need to adjust the wages of other workers earning just above lower-wage workers.

Hence, for the first three years of the scheme, higher levels of support are provided for wage increases given to workers earning up to $2,500, with some support provided for wage increase given to workers earning above $2,500 and up to $3,000.

6. Why is the minimum average gross monthly wage increase eligible for PWCS support increased from $100 to $200 starting in 2027?

To better target support for businesses that invest in their workers, the minimum qualifying wage increase for PWCS is raised to $200 for wage increases given in qualifying years 2027 and 2028.

7. Why is the co-funding level reduced from 2024 onwards?

PWCS is a transitional scheme. More support is provided in the first two years (2022-23) to help employers adjust in the short-term. Employers must take this period of transition support to accelerate their business transformation, upskill employees, and improve firm-level productivity. This is so that wage increases given to lower-wage workers remain sustainable in the long term, even after PWCS support ends.

B. Computation

1. Will employers receive PWCS support for wage increases before the new mandatory Progressive Wage Model and Local Qualifying Salary requirements start from Sep 2022?

PWCS support is given for any wage increases provided to lower-wage workers, and is not tied specifically to the Progressive Wage Model and Local Qualifying Salary requirements. Employers can raise the wages of their employees even before the new mandatory Progressive Wage Model and Local Qualifying Salary requirements begin on Sep 2022, and they will receive PWCS support as long as eligibility criteria are met.

2. If my employeeʼs gross monthly wage was reduced in 2021 but subsequently increased in 2022, will the increase be eligible for PWCS support in qualifying year 2022?

Yes, the increase in the gross monthly wage from 2021 to 2022 will be eligible for PWCS support as along as the increase was at least $100 and all other eligibility criteria are met.

3. If my employee worked for me for four months in 2022, how is his gross monthly wage and the PWCS payout computed?

His average gross monthly wage will be calculated from the total wages that you paid him in 2022 divided by 4, which is the number of calendar months in which his CPF contributions were made by you in 2022. If there is an increase of at least $100 in the average gross monthly wage in 2022 over his average gross monthly wage in 2021, you will receive the PWCS payout for the qualifying year 2022 for the 4 months.

The PWCS payout will be computed based on multiplying the co-funding level by the qualifying wage increase and the 4 months (see Computation of Progressive Wage Credit for details).

4. My employee joined the company in Nov 2021 but left in Feb 2022. Before leaving the company, he received a monthly wage increase of more than $100 in Jan 2022. As he had been employed by the company for a total of four months, will the wage increase be eligible for PWCS support in qualifying year 2022?

No, the wage increase will not be eligible for PWCS support in the qualifying year as the employee was employed by the company for less than 3 months in the qualifying year (i.e. 2022 in this case) and would therefore have not received 3 months of CPF contributions from the company.

5. My employee received a gross monthly wage increase of $200, from $2,950 in 2022 to $3,150 in 2023. Will this increase qualify for PWCS support?

The increase fulfils the criteria of having a gross monthly wage increase of at least $100. However, because part of the increase leads to the gross monthly wage exceeding the PWCS Second Tier ceiling of $3,000, only the part of the increase up to the ceiling (i.e. the first $50) qualifies for PWCS support.

6. My employee received a gross monthly wage increase of $100 that straddles the wage cut-off between the PWCS First and Second Tier, from $2,450 in 2022 to $2,550 in 2023. Will this wage increase qualify for PWCS support?

Yes, the increase fulfils the criteria of having a gross monthly wage increase of at least $100. However, while the entire wage increase will qualify for PWCS support, the increase of $50, which is up to the $2,500 ceiling, will be supported at the First Tier co-funding level, while the remaining $50 will be supported at the Second Tier co-funding level.

7. I recruited a new employee from Feb 2022 who had worked with two different employers in 2021 (each for more than three months). How will the PWCS support be computed assuming his average gross monthly wage in 2022 is $2,500 and the average gross monthly wages in 2021 was $2,000 under employer A and $2,100 under employer B?

The highest of the employee's previous average gross monthly wages, which in this case is $2,100 under employer B, will be used to compute the PWCS support.

PWCS support for qualifying year 2022 = 75% of ($2,500 - $2,100) X 11 months* = $3,300

*Assuming the employee worked with you (i.e. the current employer) for 11 months in 2022

C. Eligibility criteria

1. Are part time and contract workers covered by the scheme?

Yes, all part-time, hourly rated, contract and full-time employees can be eligible for the Scheme, as long as they are paid CPF contributions by their employer and all other eligibility criteria are met.

2. Will employers qualify for the Progressive Wage Credit for new hires?

When you hire a new employee, you will benefit from the Scheme in the year of hire if the new employee had worked for at least three calendar months with any previous employer in the previous year, and you pay him a gross monthly wage that is at least $100 more than his previous employer in the previous year.

This wage increase will be computed automatically based on the employee's CPF contribution records, and Wage Credit will be paid out to you if all conditions of the Scheme are met.

3. Will employers qualify for the Progressive Wage Credit for new entrants into the workforce?

The PWCS is purposed to support wage increases of lower-wage workers. As new entrants into the workforce do not have an existing wage (i.e. they have not received CPF contributions from a single employer for at least 3 calendar months in the preceding year), they are considered not to have received a wage increase. The wage paid by employers to these new entrants will therefore not qualify for PWCS.

4. If my employee worked for another firm in the previous year, and received a wage increase when joining my firm in the current qualifying year, will the employee’s wage increase qualify for PWCS?

Yes, even though the employee was working in another firm in the preceding year, the employee’s wage increase in the current qualifying year will qualify for PWCS as long as all other eligibility criteria are met.

The qualifying wage increase will be computed with reference to the employee’s gross monthly wage for the preceding year, that was earned at the previous firm.

5. Why are wage increases given to Permanent Residents eligible for PWCS?

The mandatory Progressive Wage Model and Local Qualifying Salary requirements are applicable to all local workers, including permanent residents. The PWCS will help employers adjust to these mandatory requirements.

D. Others

1. Do I get taxed on the payout?

The Progressive Wage Credit is a government grant that co-funds wage increases. Hence, it is considered a revenue that is taxable in the hands of the employers. The payouts will be taxed in the relevant Year of Assessment corresponding to the year you received the payouts.

Individuals (including sole proprietors) and partnerships are not required to declare the Wage Credit payout received in their income tax returns (Form B/B1 or Form P) as this will be automatically included by IRAS in their tax assessments for the relevant YA.

Companies are however, required to declare the Wage Credit payout received in their income tax return (Form C/Form C-S) for the relevant YA.

2. From 2027, the minimum wage increase eligible for support under PWCS is $200. Does this mean that firms which provide increases below $200 will not be considered to have met Progressive Wage Model (PWM) requirements, and will have their foreign worker (FW) quota impacted?

Firms that hire FWs are required to meet the relevant PWM and Local Qualifying Salary (LQS) requirements. The number of local workers that are paid at least the LQS is used to determine the firm’s foreign worker quota entitlement.

PWCS is provided as an additional support to firms that meet its eligibility criteria. Eligibility for PWCS does not affect the calculation of a firm’s foreign worker quota.